THE STRUCTURAL TAILWIND FLIPS…

Ceasefire pop, China deterioration, and why the best structural tailwind in US equities just became a headwind.

Summary: A likely ceasefire (for real this time) is juicing risk assets. Short-term indicators point to the path of least resistance being higher — for now. But intermediate and longer-term signals are flashing elevated fragility and a high probability of a cyclical top within the next 12 months. Warsh’s first FOMC this week should give us a read on how willing he is to look through inflation. Bonds and USD continue to compress, setting up for major trend breaks. China’s financial conditions are deteriorating fast. Net equity supply in the US just flipped positive for the first time since COVID. Earnings estimates are likely to disappoint. Plus a long equity play.

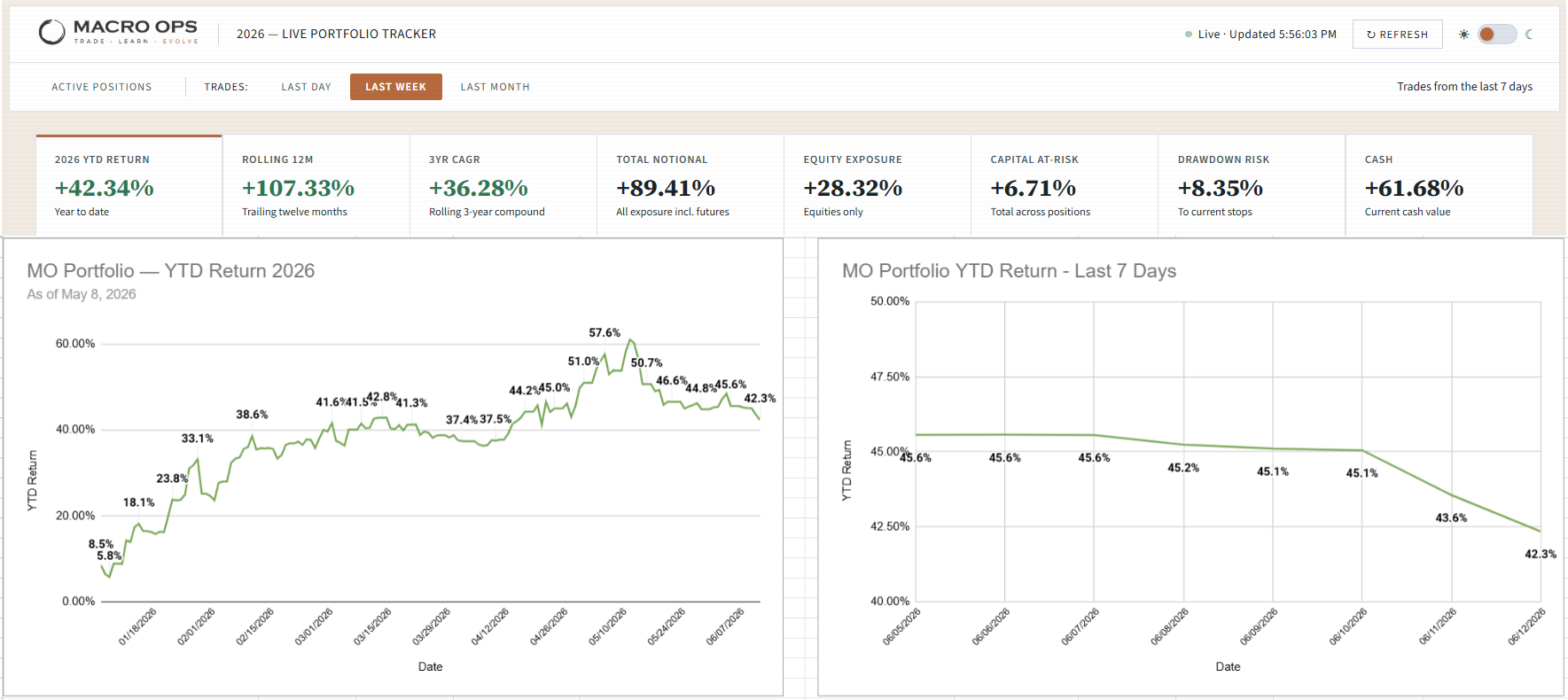

MO Portfolio & Trades

1. The portfolio ended last week down 330bps, bringing year-to-date returns to +42.3%, below our YTD NAV high of +61%.

Current positioning: elevated cash, select beaten-down software, healthcare, and cybersecurity names; short ETH; long gold miners; long the Bloomberg Commodity ETF; a handful of idiosyncratic equity positions.

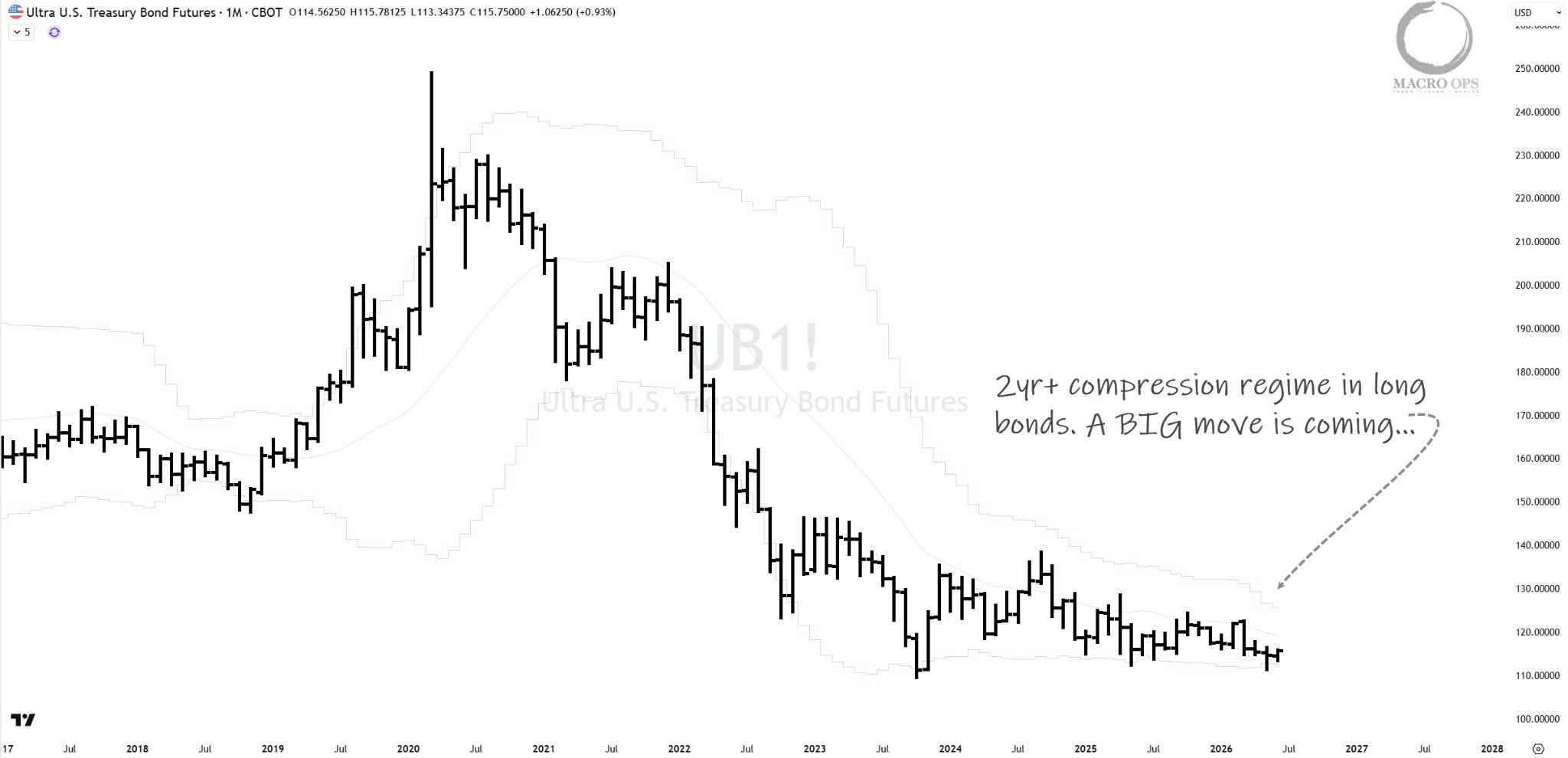

2. Will keep posting this one weekly as it’s one of the most important setups in macro right now and is gearing up for a big move.

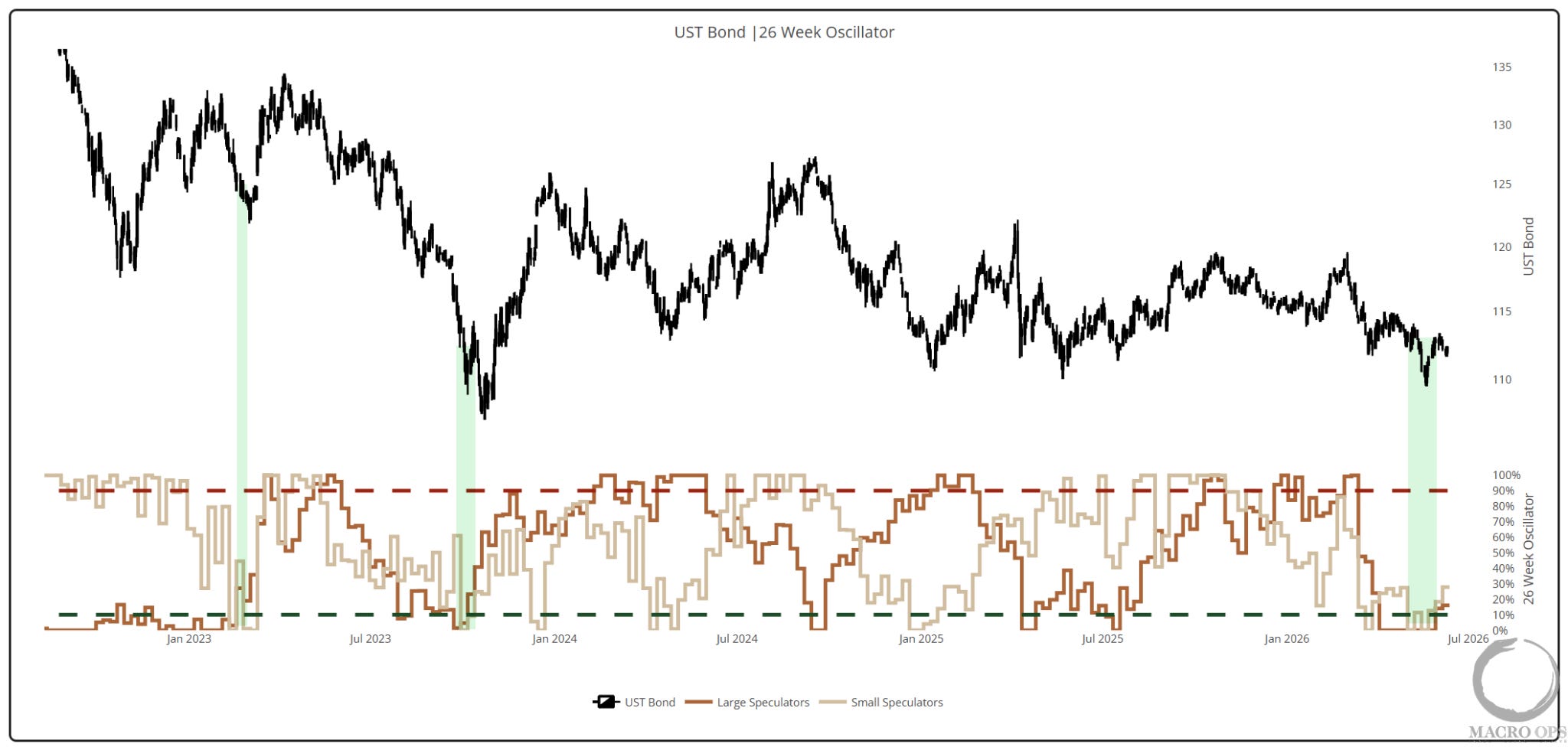

3. Our 26 week positioning oscillator is climbing up from below the 10th %tile, showing crowded bearish positioning and giving us a long setup to play for reversion back to the middle of its compression regime.

4. Similar to long bonds, the DXY chart is one I’ll keep showing each week until we get a breakout. Last week I pointed out that yield spread momentum and positioning were similar to the conditions that preceded the 21’ rally in USD. We’ll see if a budding speculative frenzy in the US can catalyze a bullish breakout from this range.

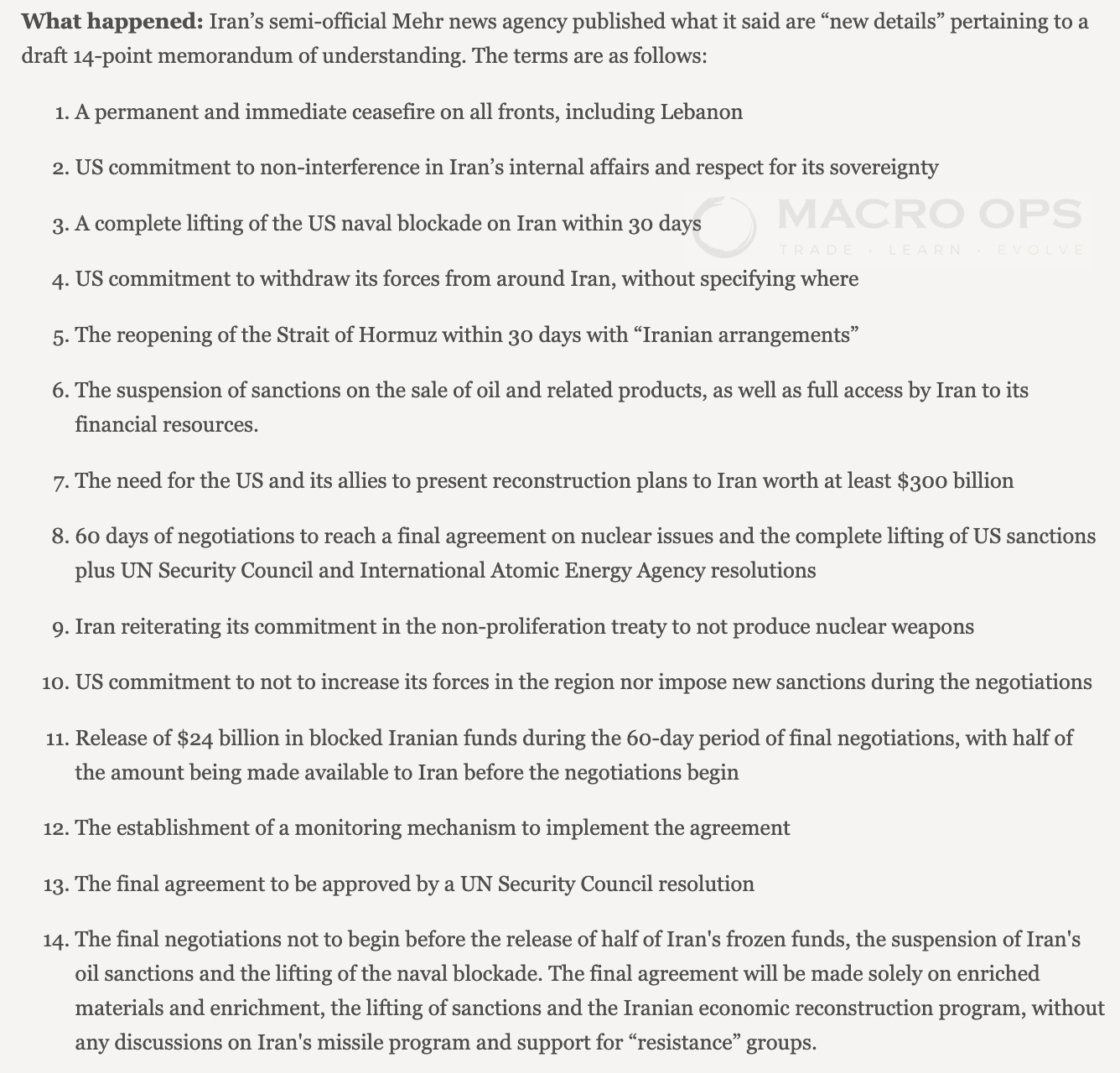

5. If even half the points in this Iran-US draft deal circulating on Iranian state media are real, it amounts to total US surrender. Trump wants out. Midterms are the focus now(link here).

6. Crude getting smoked on the news. And no surprise, the specs who we faded at the lows around the turn of the year find themselves completely offsides once again. It’s almost like there’s something to this positioning thing.

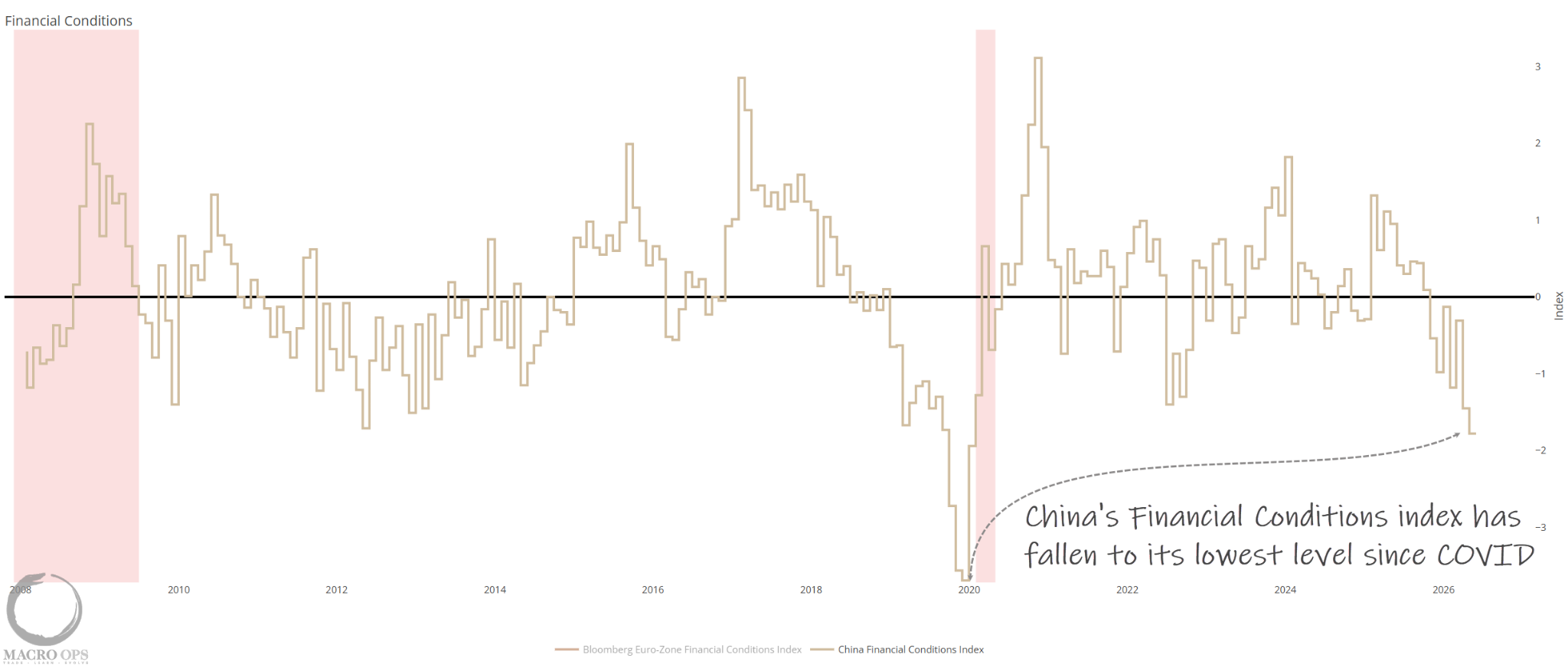

7. What’s going on in China? China’s Financial Conditions Index is falling to levels not seen outside of COVID.

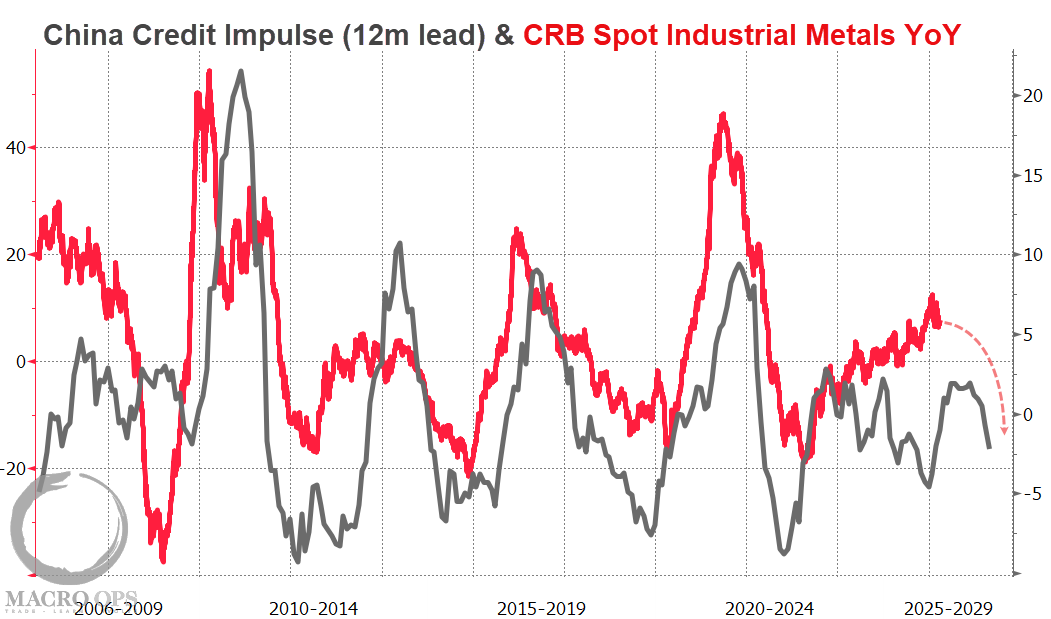

8. Credit impulse is back in negative territory and trending lower. Historically, this has been a strong lead indicator for commodities, particularly industrial metals. The AI buildout may make that relationship more spurious going forward. We’ll see.

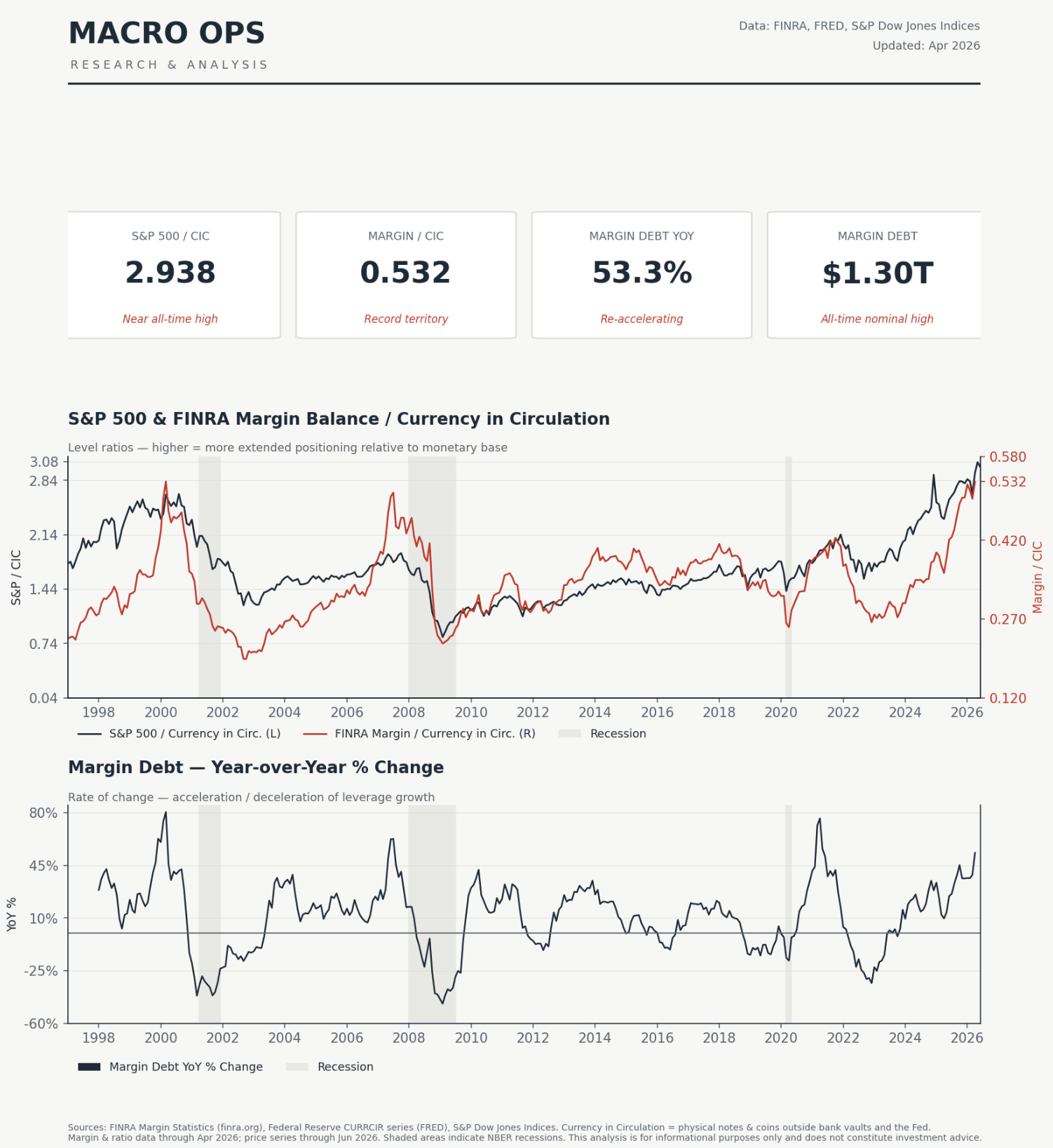

9. I flagged this chart at the start of the year: NYSE FINRA Margin Debt was elevated at 35% YoY but still shy of concern territory. It’s now approaching that threshold. On a margin balance-to-currency basis, it’s at dot-com highs. On a YoY basis, it’s risen to 53%. An official sell signal triggers above 60% then reversing below 50%. How fast we get there depends on the market path — but with midterms in November, I’d expect the administration to pull out all the stops.

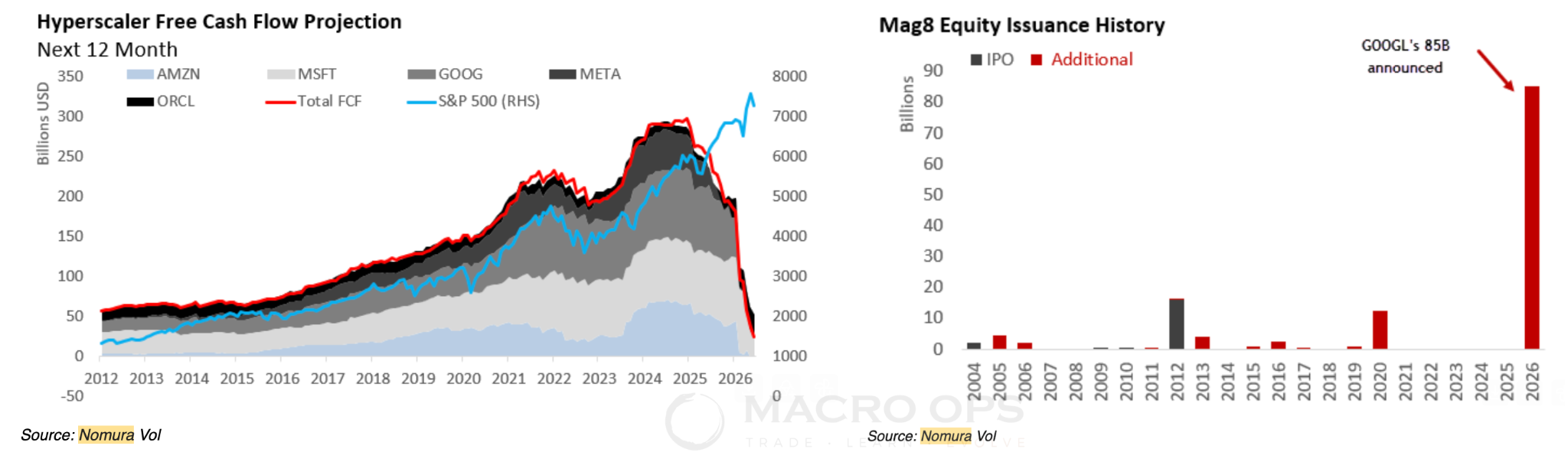

10. Nomura’s Charlie McElligott on the MAG7 becoming funding sources for the next leg of the AI trade:

As somebody who is “medium horizon” (next two-three quarters) constructive on AI Capex trickle-down and US Equities (Earnings Growth Tailwind broadening out from the Capex boom uplift i.e. Manu mini-renaissance), the LOCAL issue I see for US Equities Index now is that we almost certainly CANNOT resume making new highs without the Mag7 Hyperscalers doing the heavy lifting, as they’re simply “too big” and matter too much, particularly with regard to 2nd order impacts on both “Real and Synthetic” Negative Gamma forces in the market (i.e. the recent pro-cyclical “Spot Up, Vol Up, Crash Up” regime via Options Upside Call demand and Leveraged ETFs) which HAD propelled us higher in what HAD been a 3 Sharpe 3m move

So how is it that now Hyperscalers have tilted into what I believe to be a broad Equities market HEADWIND? It’s really two-fold:

In some ways, the Hyperscalers and big Semis / GPU -plays are now closer to acting like the FUNDING SHORTS in the maturation in this “AI Trade” phase-shift…as the opportunistic Longs have moved OUT OF the “Perpetual Capex Spend Arms Race” and first-order “Winners”…and instead, down the stack into the “Bottlenecks” of Memory, Silicon, Infra, Servers, Networks, Robotics etc…in other words, Hyperscalers and Semis are increasingly looking like “Source of Funds” in the trade

But in addition to this aforementioned phase-shift / maturation of the AI Trade…I have to pound the table on the point I made Sunday night in the email, which is this idea too that the Hyperscalers are at the core of this potential paradigm shift in “Supply > Demand” in Stocks, AWAY FROM what had been the virtuous 15+ year “De-Equitization” -period for US Stocks, where the Float had been shrunk and Vol was suppressed as a massive tailwind for Stocks on account of the unprecedented “Demand > Supply” flow realities this created via “Buybacks + Cash M&A > Issuance”

But now into this new world order of what feels like as “Exponential” Capex funding needs, Cash is being burned through at “known unknown” rates of speed vs Spend plans, which is then not only endangering the “Flow” of the Stock Buyback “Demand”...

…While at the same time, we have this “Supply Overload” issue: Not just the overall Equities issuance “Cannibalization” risk of more need for “Funding” via the sheer $size of the tectonic Mega Tech / AI -linked IPO calendar coming in a tight window, which is why there’ all eyes on how SPCX takes Friday and thereafter…but critically too, the Hyperscalers’ OWN SUPPLY from issuance now acts like de facto “Overwriting” of themselves (as if they were selling Long-Dated Calls), with the risk of “Issuance Overhead” helping to further “Kill Off” the “Spot Up, Vol Up” residuals, after last week’s massive GOOGL $85B ATM offering, and the ensuing reports that META would be looking at potentially doing the same

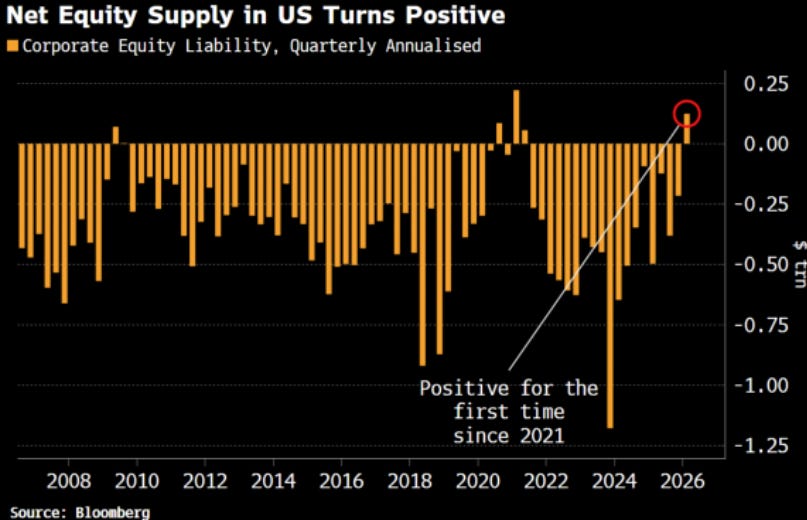

11. One of the structural tailwinds for US equities has been net share cannibalization — US companies have been buying back more shares than they issue, creating persistent demand against a shrinking float (more on that here). That dynamic just flipped positive for the first time since 2021, and with the coming wave of mega IPOs and megacap issuance, it’s likely to stay that way for the next 12 months. A structural tailwind is now a headwind. (Chart via BBG’s Simon White.)

12. Expected operating margin growth is running well ahead of revenue expectations — the market is front-loading a lot of AI-induced productivity. That’s a crowded bet.

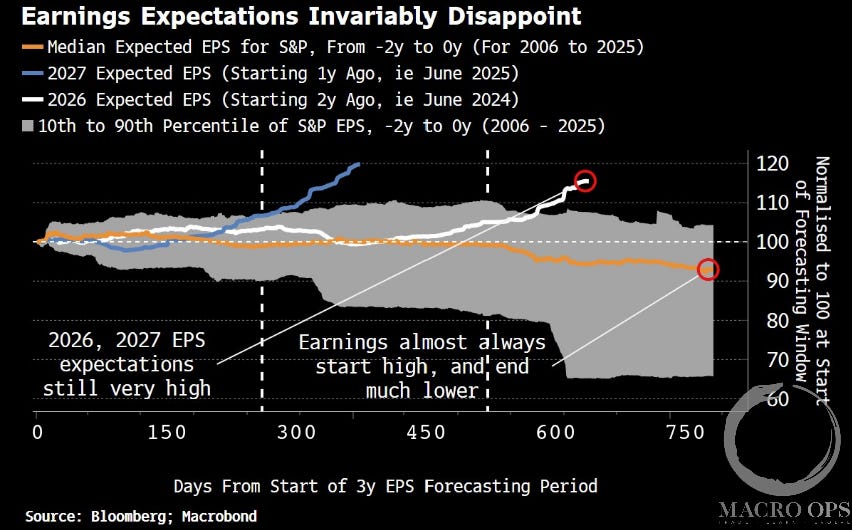

13. Simon White shows how elevated earnings expectations tend to mean-revert as we move through time.

14. Again from Simon, this is a great chart…

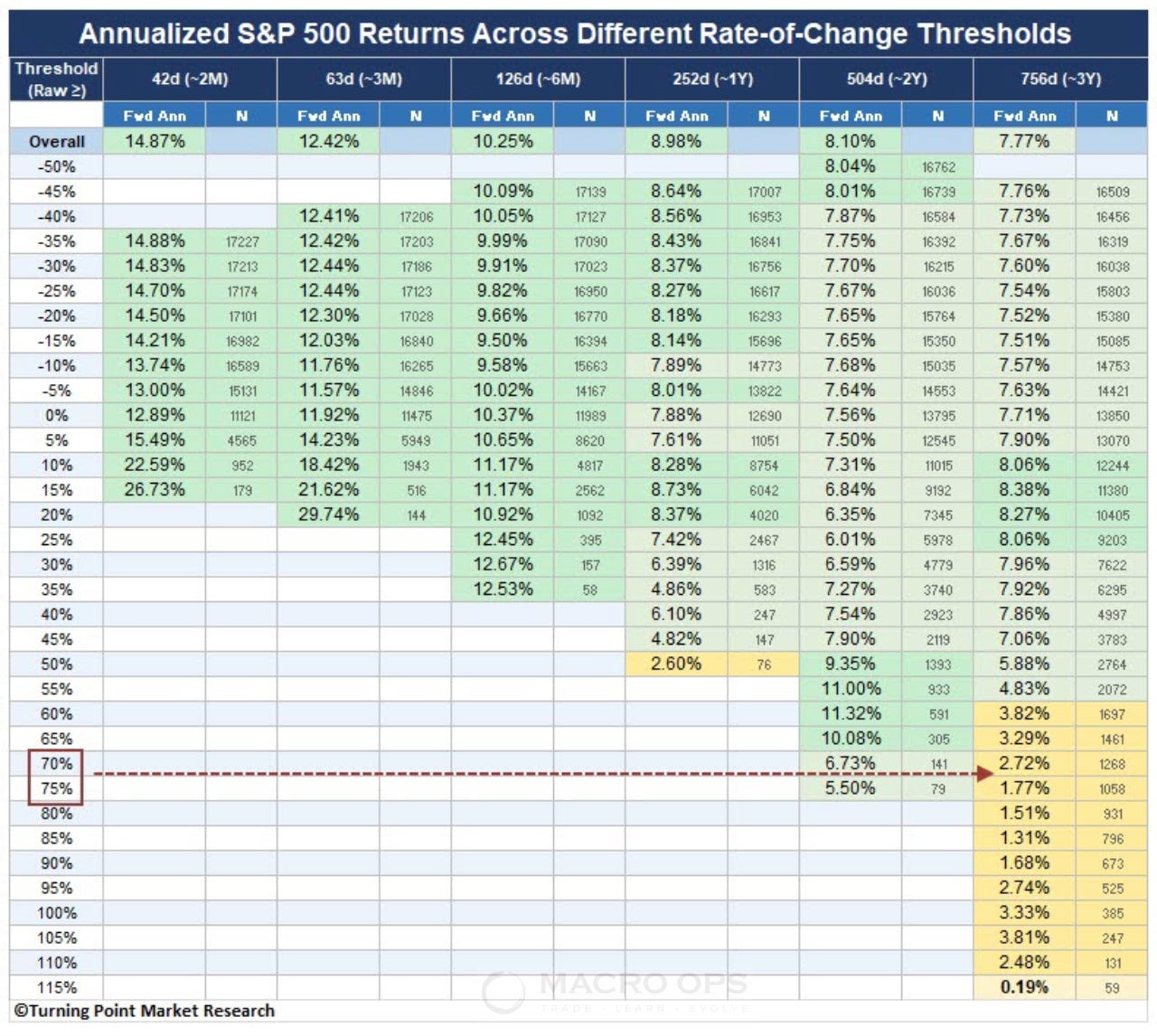

15. This is an interesting study from our friend Dean at TPMR (link here). He writes “The S&P 500’s three-year rate of change recently peaked above 84% and currently stands at 72%. Readings in this range have historically been associated with below-average annualized returns, as shown in the table below. However, I would note that shorter-term readings continue to reflect positive momentum, which is generally bullish.”

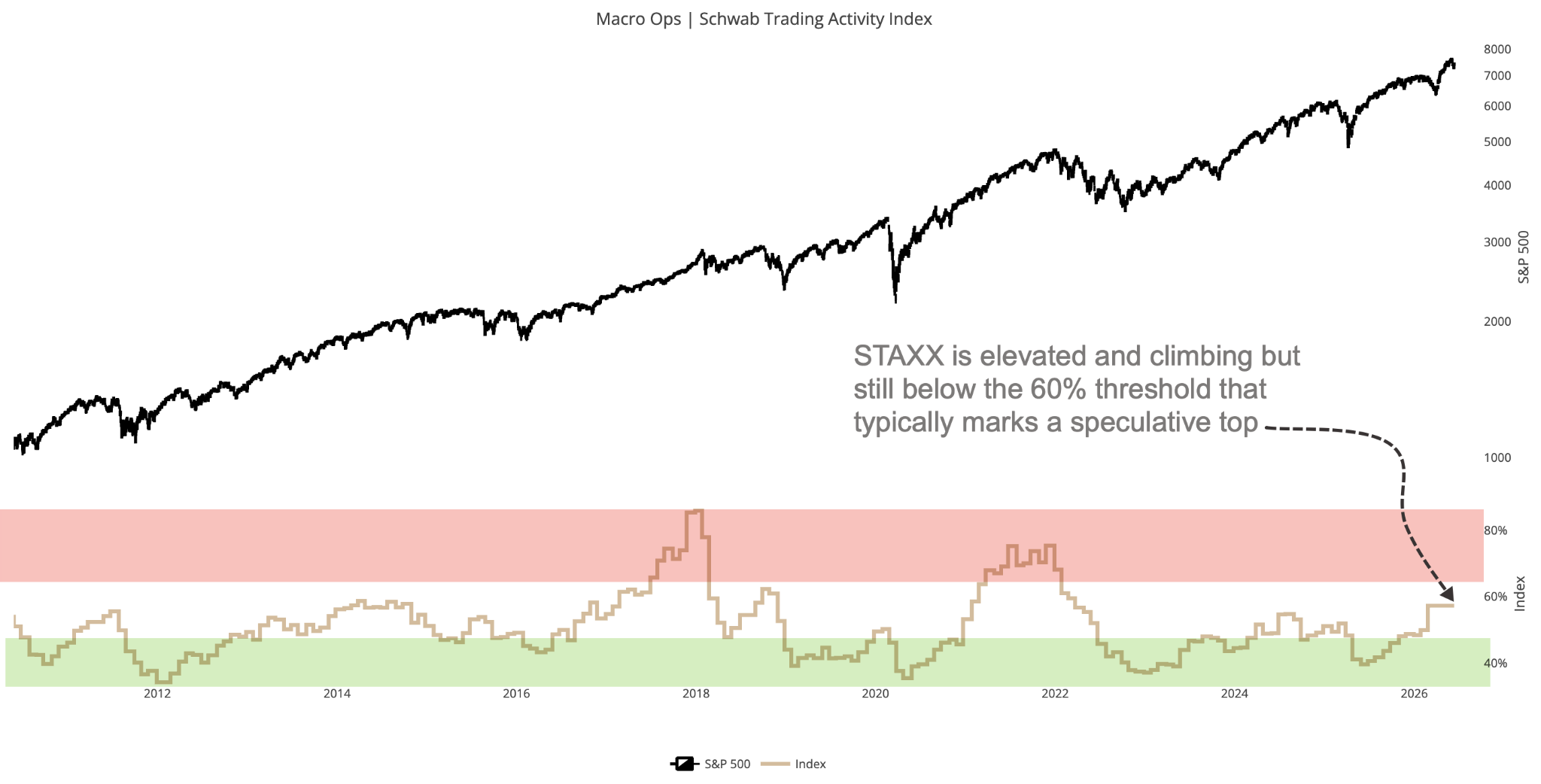

16. So things are getting frothy, sure. But interestingly one of our favorite intermediate term indicators of retail speculation, the STAXX index which measures millions of actual retail positioning and flows, while elevated, is still below the 60% threshold that tends to mark speculative peaks. Like margin data, we’ll likely see this signal trigger in the coming six months.

17. The Qs held their breakout level last week. We are long.

18. SII is a geared play on a structural bull market in precious metals and critical materials. AUM is already compounding off gold, silver, uranium, copper, and energy transition themes. If you believe in currency debasement, central bank gold buying, and capex-light green/AI infrastructure buildout, Sprott’s platform gives you a clean way to express that view — with growing fee streams and dividends. It’s teeing off its lower weekly band and 200dma.

Thanks for reading.

Your Macro Operator,

Alex