“It is impossible to produce a superior performance unless you do something different from the majority” – Sir John Templeton

This will be a quick Long Pull as I’m prepping for tomorrow’s MOHO Idea Lunch with @Tobias. As usual, we will record the webinar, so don’t worry if you can’t make it.

We’re doing podcast notes, people! I know, I’m finally doing it this year after three years of Alex asking why I never did them. Better late than never.

Oh, before we dive into the Podcast Notes, I want to let you know that we’re still accepting Collective member sign-ups.

The MO port finished 2025 up +50.8% and is currently up 28%+ ytd in 26’.

If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click below and sign up.

We look forward to seeing you in our Slack!

Podcast Notes: Tim Call – Capital Management Corporation

Last week, I interviewed Tim Call of Capital Management Corporation. Tim is a stereotypical value investor.

He focuses on “growing cash cows” through analyzing operating and free cash flow. He invests in niche leaders that exhibit growing free cash flow and increasing GAAP earnings (Tim emphasized GAAP earnings on the podcast, which I deduced as a disdain for things like SBC, etc.).

The “niche leader” part is important because you don’t always think of small caps as “niche leaders.” Leaders should be multi-billion-dollar businesses in large industries. It reminds me of the book Hidden Champions, which profiled a bunch of companies that stayed small to dominate their little niche.

Which company would be the value trap? An “optically cheap” small-cap company fighting for its life in a large industry? Or an equally cheap small-cap company dominating its small corner of a small industry?

We can distill Tim’s investment framework into four main criteria:

Small- to mid-sized company ($80M to $10B, according to Tim).

Generating positive free cash flow with a history of FCF growth.

Trading at a cheap valuation relative to GAAP earnings and normalized FCF.

Niche leader in its category.

Idea Generation, Portfolio Management/Construction, & Diversification

Tim’s idea generation process is so different from mine. He has a predetermined list of ~3,000 companies to choose from. I know that sounds like a lot. But there are 54,000+ stocks globally.

While part of me hates that idea, another part of me loves it. I struggle with the Paradox of Choice. Having the ability to invest in 54,000 different companies sounds like freedom. But it’s paralyzing. It’s one of the reasons I’ve switched to the RS Inflection/Composite monitors: I can focus on just a few industries.

Tim further narrows that list by selecting profitable companies with a history of growing FCF and GAAP earnings.

Let’s talk position sizing and portfolio construction. According to Tim (emphasis added):

“Full positions are historically 4%, though they may go up to 5% in regular portfolios for new money or existing value in extreme situations, and higher in concentrated specialty portfolios.”

This means Tim has a portfolio of ~20-25 stocks, with the majority of the portfolio weighted in the top 5-10% companies. Remember, Tim only wants to invest in niche leaders, which naturally reduces the number of companies you can own (emphasis added):

“We focus on the ‘best of the best’ and maintain great diversification by seeking niche leaders, which naturally limits the number of companies in any one category.”

Alright, let’s get to the ideas.

Idea 1: Lifevantage Corporation (LFVN)

Market Cap: $78M

Enterprise Value: $65M

Normalized FCF: ~$10M

P/E (NTM): 5.5x

EV/Sales (NTM): 0.3x

Latest Investor Deck: December 2025

What does the company do: LFVN engages in the identification, research, development, formulation, and sale of advanced nutrigenomic activators, dietary supplements, nootropics, weight management products, pre- and probiotics, and skin and hair care products. Think Herbalife (HLF), but for antioxidants, gut peptides, collagen-based products, and GLP-1s.

The Bull Thesis: LFVN produces immense cash, is debt-free, and trading at a single-digit P/E on GAAP earnings. The company has initiated and annually raised a dividend, and is buying back stock after funding internal growth and paying off all debt.

The Bear Thesis: Lingering concerns about the rise of strong substitute products like diabetes drugs approved for weight loss, and the possibility of mistaken identity with volatile stocks like LifeMD (LFMD).

The Rebuttal To The Bear Thesis: LFVN is more focused on overall health, including gut health and metabolism, areas that the new drugs may not necessarily address. The company is expected to increase cash flow and earnings growth through new product introductions, geographic expansion, and a recent acquisition that added both a product and a sales force.

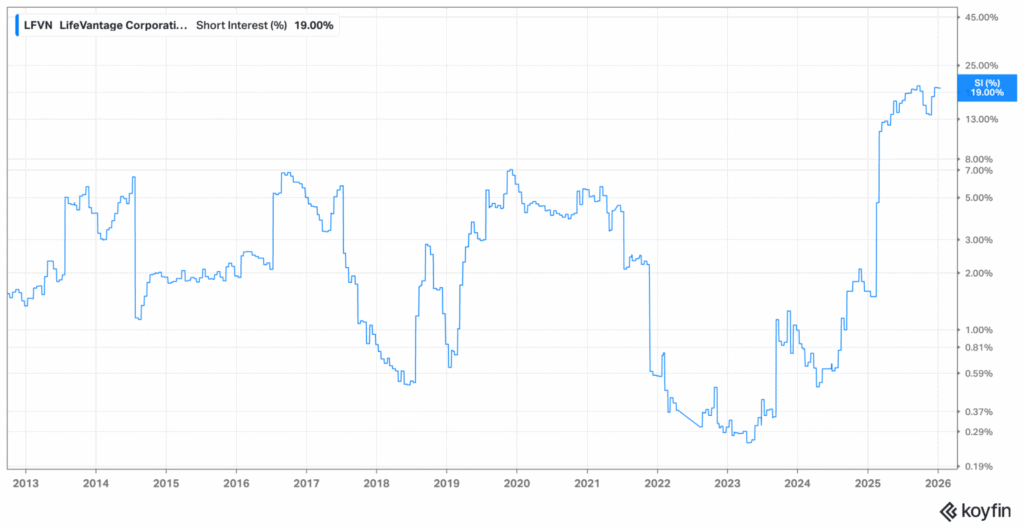

The Short Interest Kicker: LFVN has a 19% short interest as of this writing. This caught my attention. Why would a company, which generates $10M+ in FCF/year with no long-term debt and a history of shareholder returns (dividends + buybacks), have that high a short interest?

Usually, you’d see a few short reports on a company with that high a short interest. But nothing on VIC or Seeking Alpha (see below).

I even tried Googling “Lifeadvantage short report” and found nothing.

My explanation for the short interest is that LFVN operates a “multi-level marketing” business model (again, like HLF). Most investors hate these businesses for the obvious reason: bad optics.

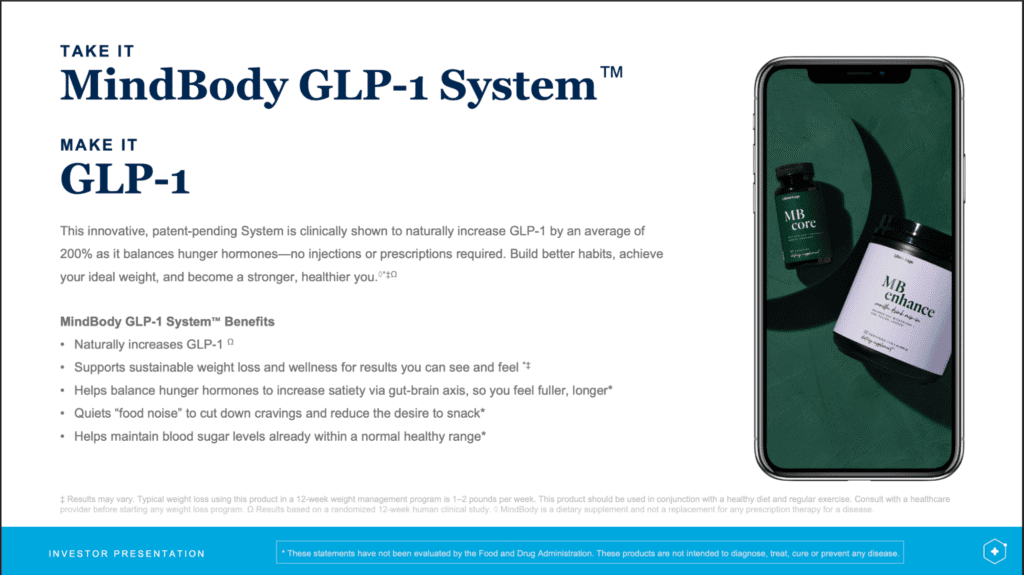

And maybe they’re short because GLP-1s will destroy LFVN’s business and products over time. But I don’t know. The company recently released a GLP-1 product to “naturally increase GLP-1 by an average of 200% as it balances hunger hormones—no injections or prescriptions required.”

The company is also entering the $32B gut peptide market, which different corners of “Health Twitter” have called “Vibe coding for your body.”

There are challenges:

Top-line revenue has been stagnant since 2019.

Gross margins have declined from 83% to 80% (still excellent).

SG&A remains 75% of revenue (part of the MLM model).

For example, why does HLF have 10% EBITDA margins when LFVN has 5%? What is HLF doing with their MLM that LFVN isn’t (or can’t?)? Is there an opportunity to expand EBITDA margins? Or is that a byproduct of a worse business model and product category?

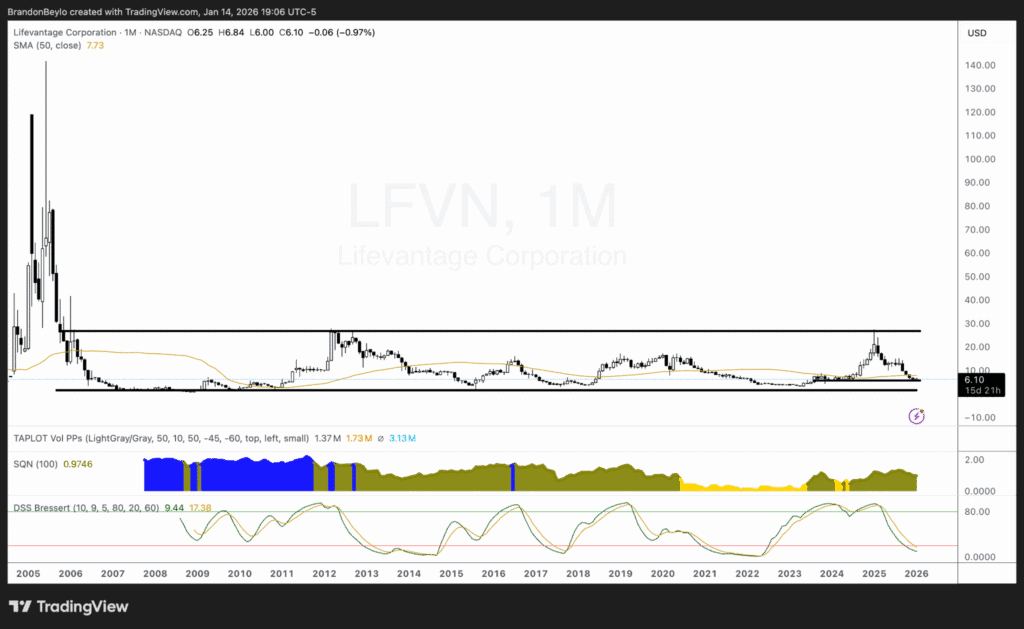

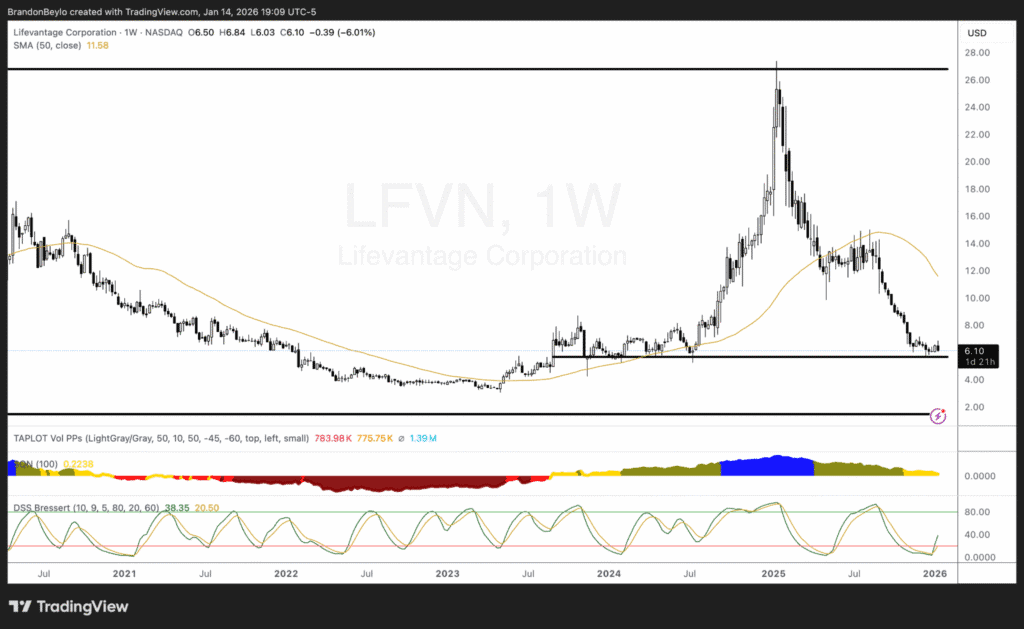

Let’s head to the chart.

The stock trades towards the lower range of its twenty-year base, and the DSS Bressert Signal is below the red (oversold) line. Zooming in on the weekly chart, the stock bounced off two-year support with a confirmed Bressert Buy Signal (see below).

Idea 2: Acco Brands Corporation (ACCO)

Market Cap: $360M

Enterprise Value: $1.24B

Normalized FCF: ~$133M

P/E (NTM): 3.8x

EV/Sales (NTM): 0.2x

P/B (LTM): 0.6x

Latest Investor Deck: October 2025

What does the company do: ACCO designs, manufactures, and markets consumer, school, technology, and office products in the United States, Canada, Brazil, Mexico, Chile, Europe, the Middle East, Australia, New Zealand, and Asia.

The Bull Thesis: ACCO underwent a multi-year reorganization under new management to shift from low-margin to value-added products, navigating temporarily reduced earnings during the process. The thesis includes an expected sales boost from a computer refresh cycle and the launch of Nintendo Switch 2 accessories, which should improve earnings in the fourth quarter.

The Bear Thesis (as I see it):

Consistent revenue decline: Three straight years of declining revenue.

EBITDA margin compression: From 15% to 10%

Secular headwinds: Mature and declining end markets with pressure from hybrid/fully-online programs (reducing brand dependency with school relationships).

Commoditized products: Do you really care what brand of stapler you buy?

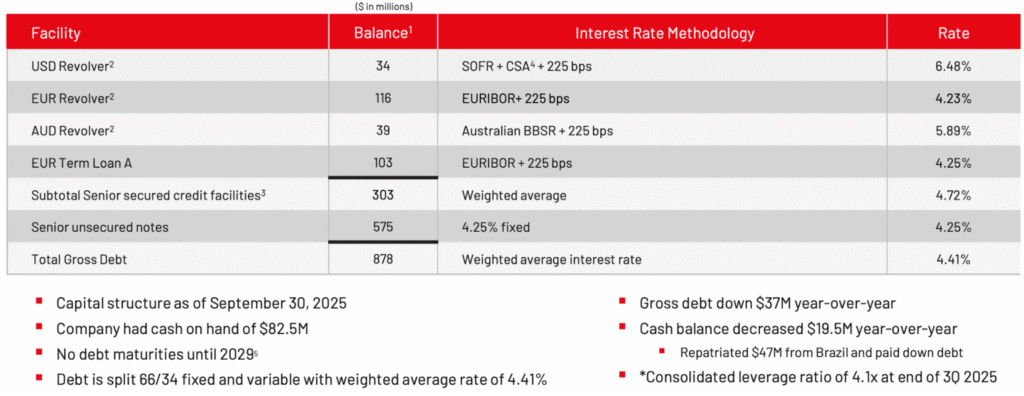

At its current price, the market thinks ACCO will eventually declare bankruptcy (0.2x sales and 0.6x book). That makes sense on the surface … $360M market cap with $1.24B in EV ($880M in net debt).

However, as Tim explained (emphasis added):

“The debt is down from 2021. The market also doesn’t appreciate ACCO’s ability to easily refinance and has no maturities until 2029. The company is focused on debt paydown but has also used cash for share buybacks, which reduced dividend expenses, and currently offers an 8% dividend yield.”

Despite its significant net debt, ACCO has consistently returned cash to shareholders. Since 2018, the company has paid cumulative dividends of ~$208M and repurchased $233M in stock.

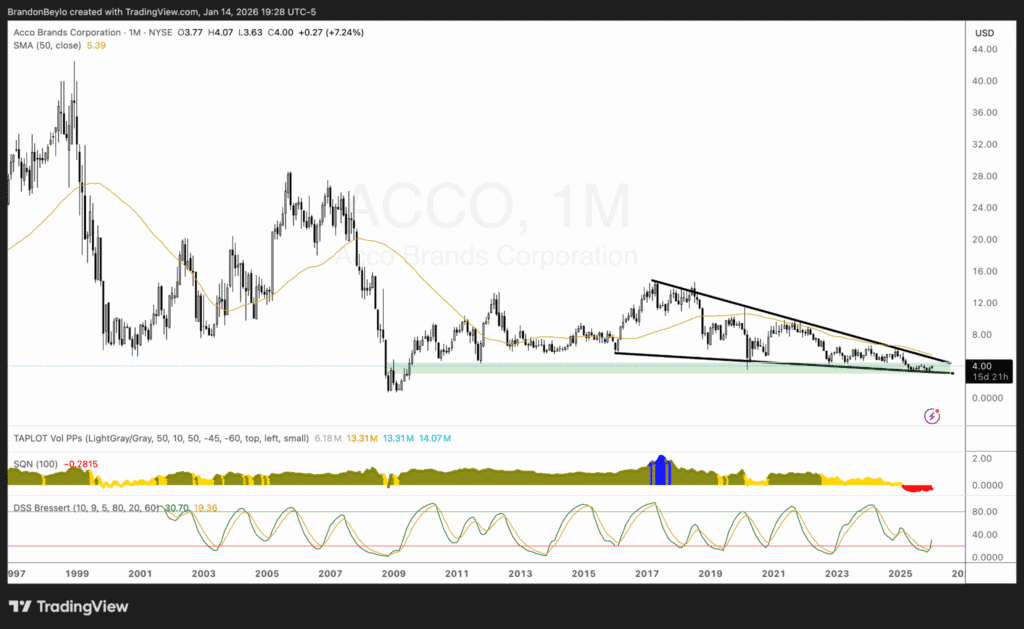

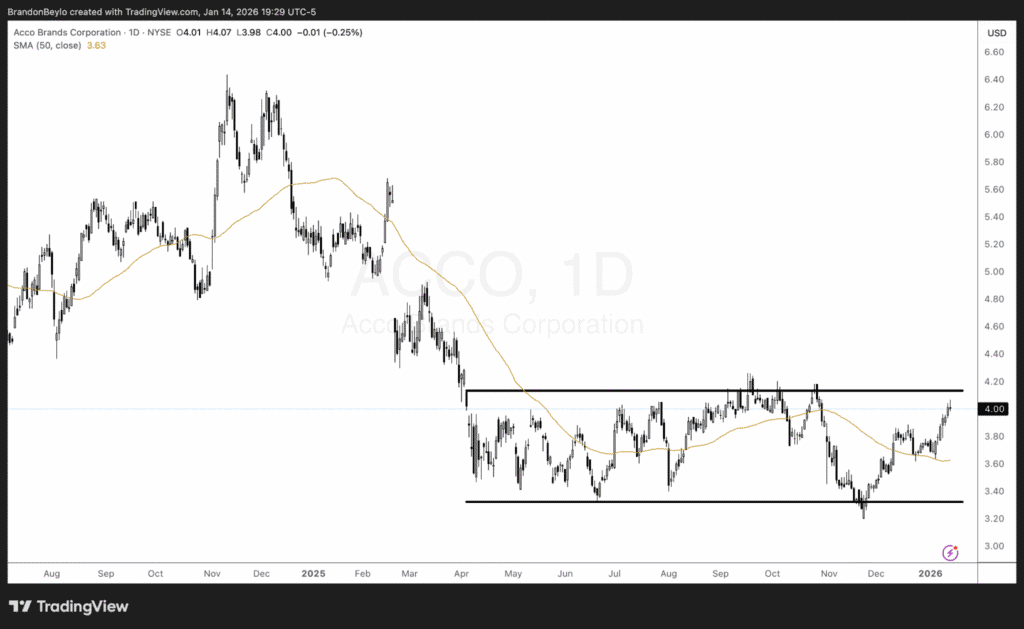

Let’s head to the tape.

We have a potential Bressert Buy Signal on this month’s bar, in a descending wedge pattern at long-term support.

You can also zoom into the daily chart and find a textbook rectangle reversal pattern (see below).

I’m Fishing In The Right Ponds

I like both setups, but prefer LFVN because it has no debt and operates in an industry that a) I like more and b) has more secular growth potential.

The other great thing about these ideas is that my screeners already found them. For example, LFVN was in my “Stupid Cheap” and “The Worst of The Worst” screeners as of 01/03. And ACCO fit the “Left For Dead” and “Cheap Vs. Own History” screeners.

I’m fishing in the right ponds and filtering for the right companies based on Tim’s (and the Trifecta Lens Mean Reversion) strategy. That’s encouraging.

I hope you enjoyed these Podcast Notes. Excited to share more of them with you this year.

Impressive how LFVN maintains 19% short interest despite strong FCF generation and no debt. The MLM optics angle makes sense as an explainer but that GLP-1 product launch timing is fasinating. Looks like they're trying to ride the wave instead of geting crushed by it, which is smarter than most supplement companies are doing right now.