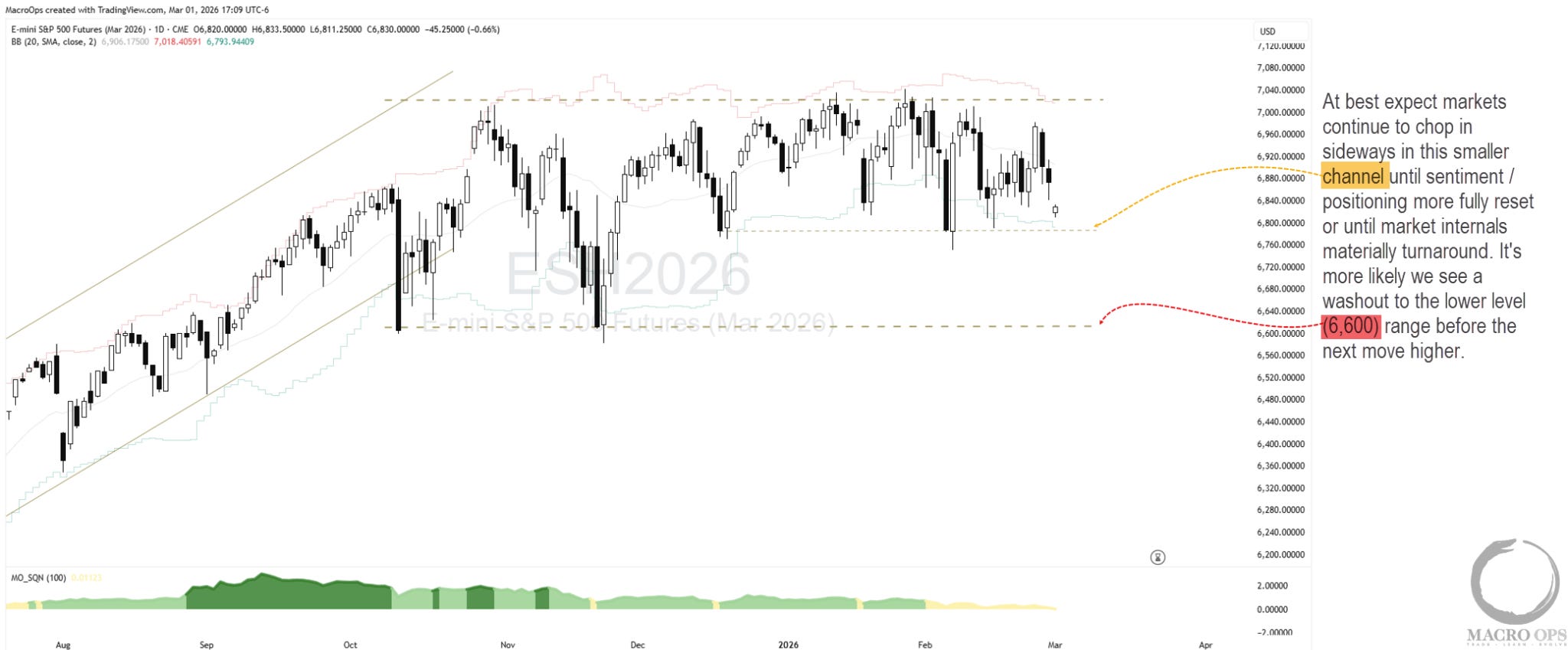

Summary: Sentiment and positioning are slowly resetting — but they still have a ways to go before we can call it a true reset. Market internals are deteriorating fast, which historically points to poor 1-month forward returns. Expect continued sideways chop and vol in the indices; SPX likely retests its November lows before all is said and done. That said, there’s plenty of action elsewhere. Our focus remains long oil, long the front end — and now potentially short the long end for some curve steepening. We close with a revisit of a biotech name that continues to show strength.

MO Portfolio & Trades

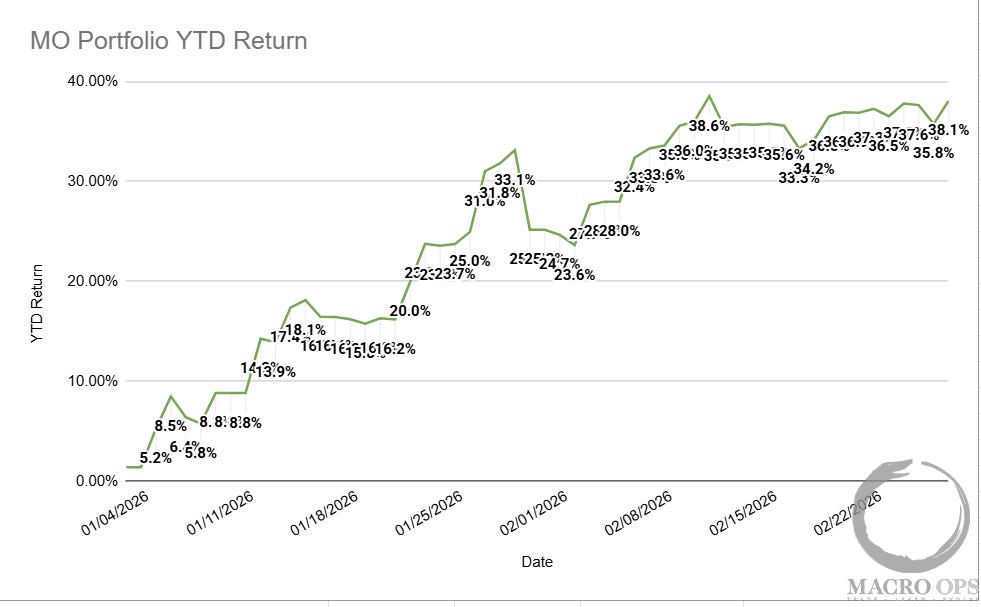

1. The MO portfolio gained +90bps last week, helped by our silver and miners longs. It’s now up +39.58% ytd. We’ll see where things open Monday, but I’d expect our long oil calls to be up nicely.

If you’d like to join our Collective and have access to our research, tools, Slack, and the team and me, just click here.

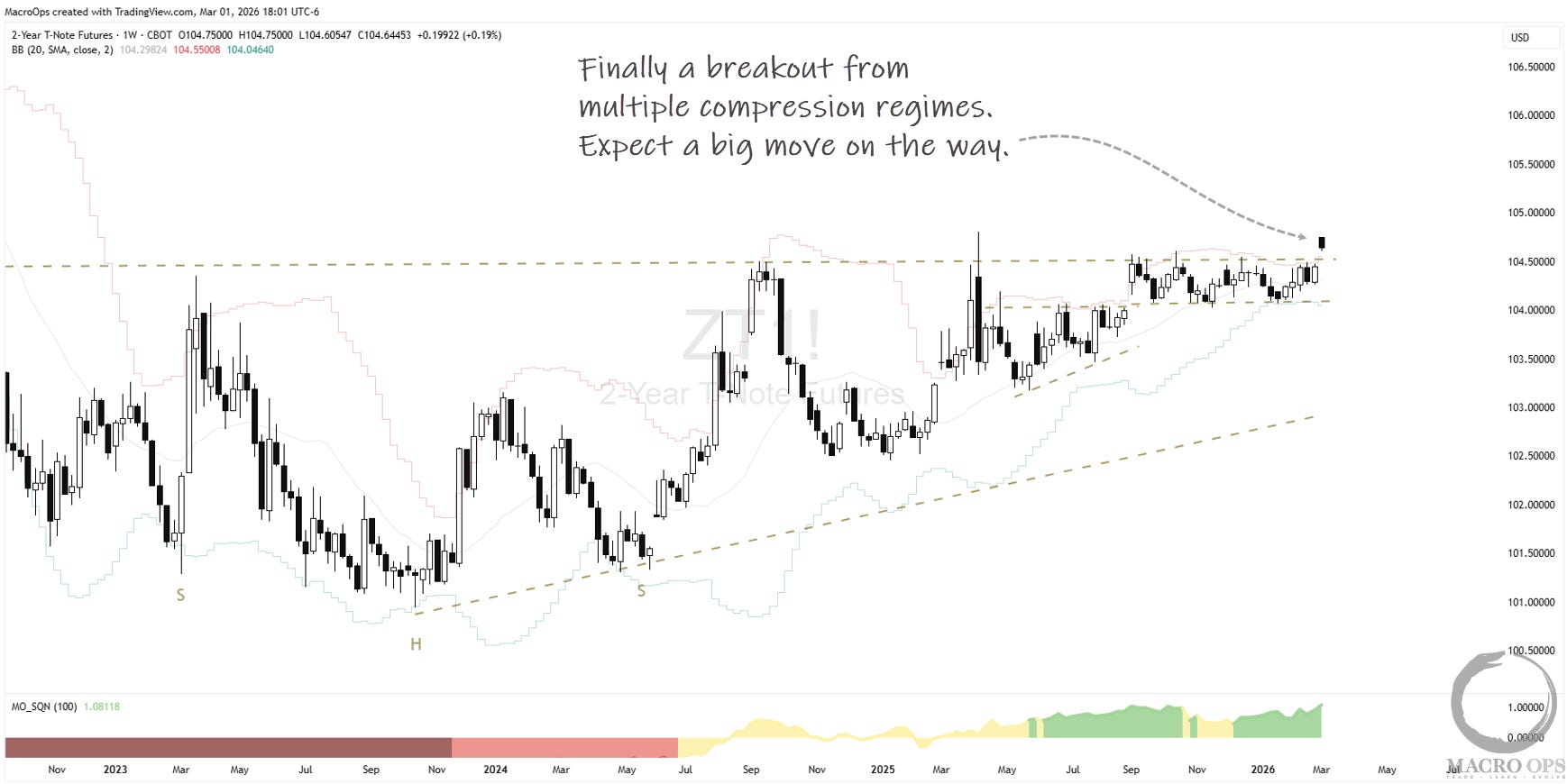

2. We’ve been stalking this multiple-compression setup in 2-yr T-Notes for months, and it looks like we’ve finally gotten a breakout. We’re already quite long, but we’ll look to add as long as this move holds and the tape stays firm.

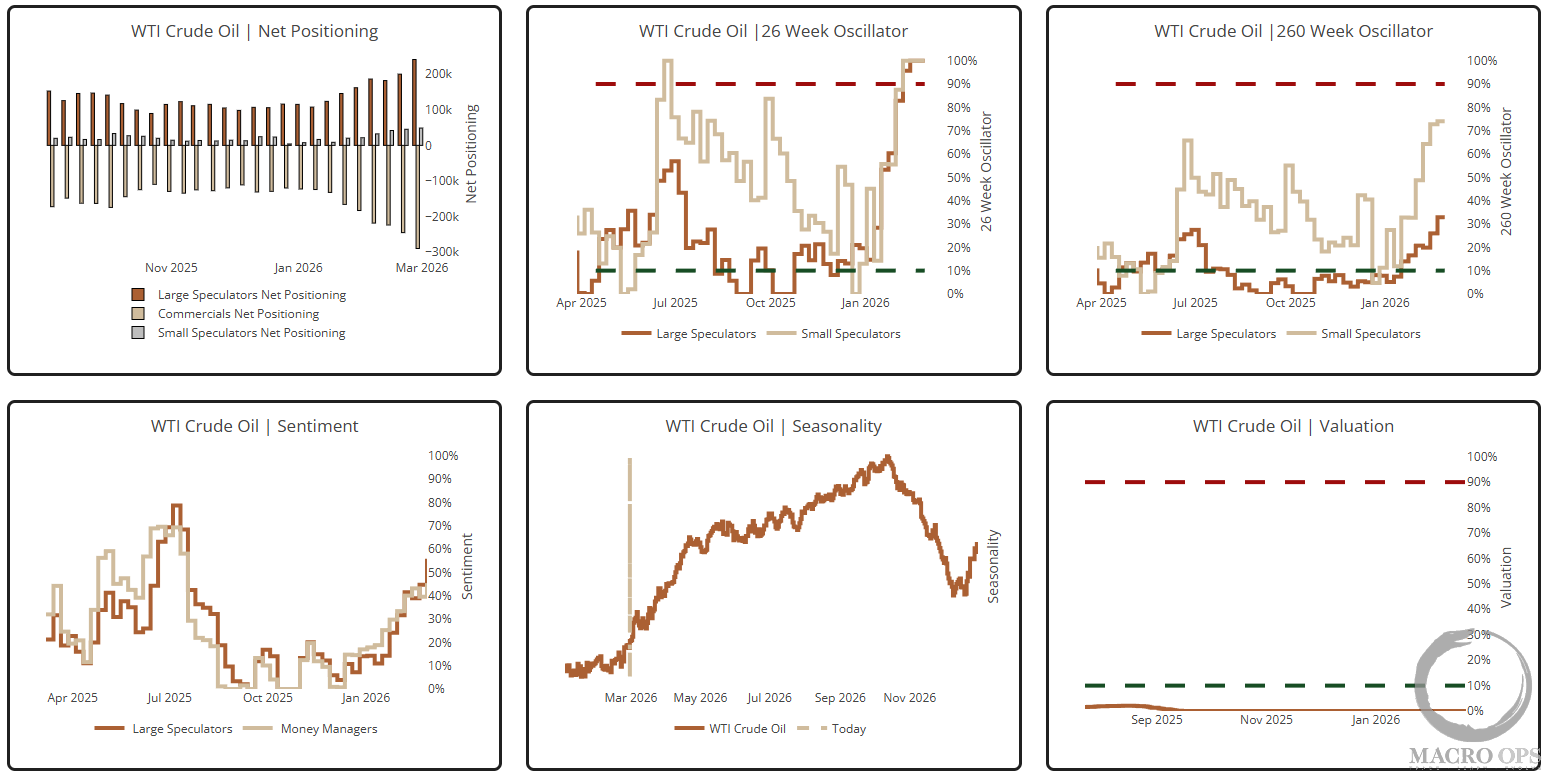

3. Last week I reiterated the Trifecta (macro + positioning + technicals) setup in crude, along with the likely positive catalyst of an attack on Iran (link here). We’re heavily long the futures and equities and think this trade has legs. Short-term positioning is shifting fast (26-week oscillator below), but it’s coming off a historically pessimistic base. Seasonality is very favorable, and crude’s relative valuation sits at the 0th %tile.

Trifecta Charts

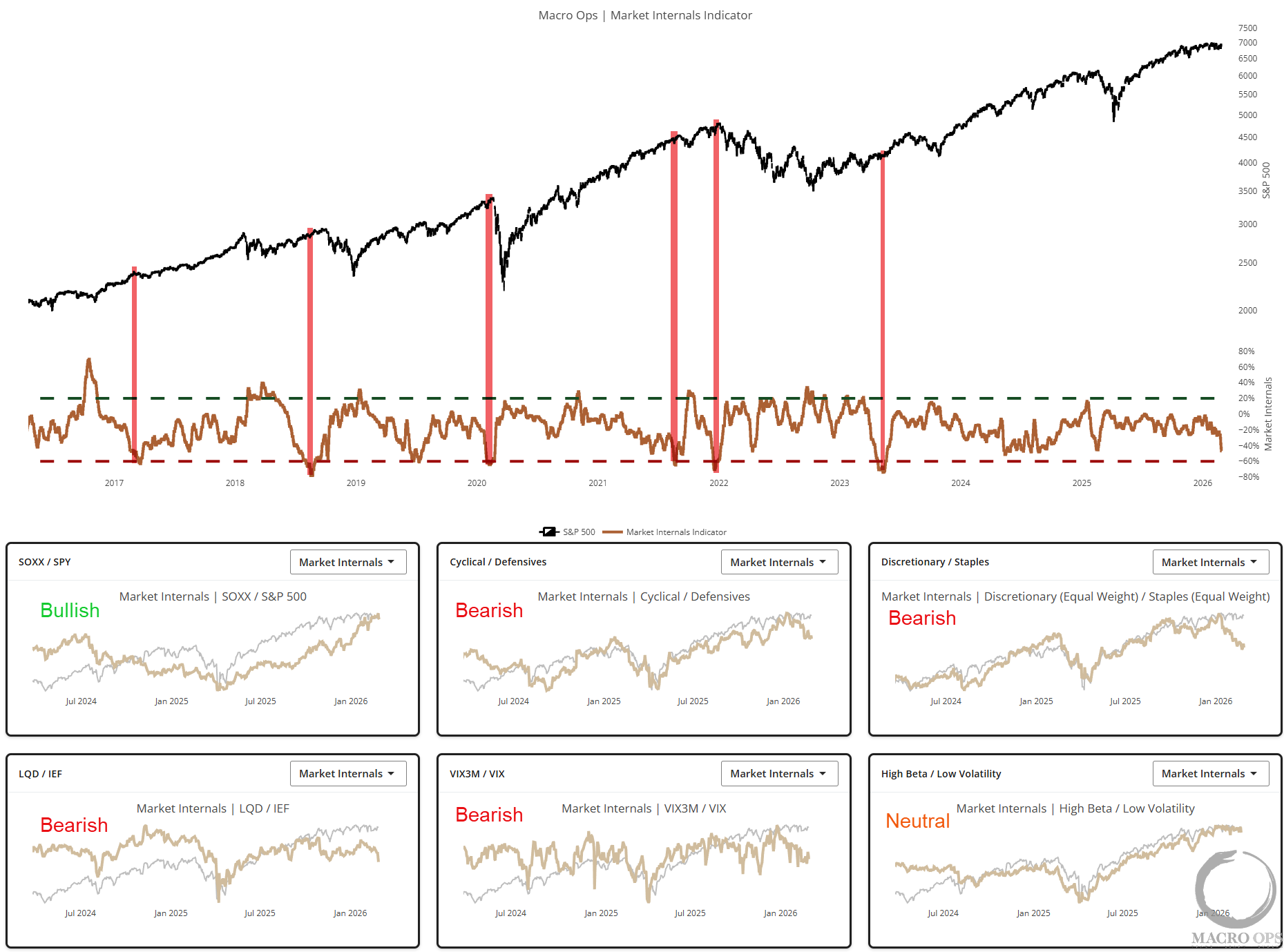

4. Our Aggregate Market Internals indicator is in nosedive mode. Not quite at official sell signal levels yet, but it could trip there this week — worth watching closely.

5. We still don’t see broad weakness in aggregate breadth, so we can’t turn outright bearish. The full Trifecta picture continues to suggest more chop and vol in the main indices, with risk skewed to the downside. SPX likely retests its Nov ‘25 lows — but this will probably be a grinding move rather than a cascade, as rotation flows and flush liquidity keep other pockets of the market bid.

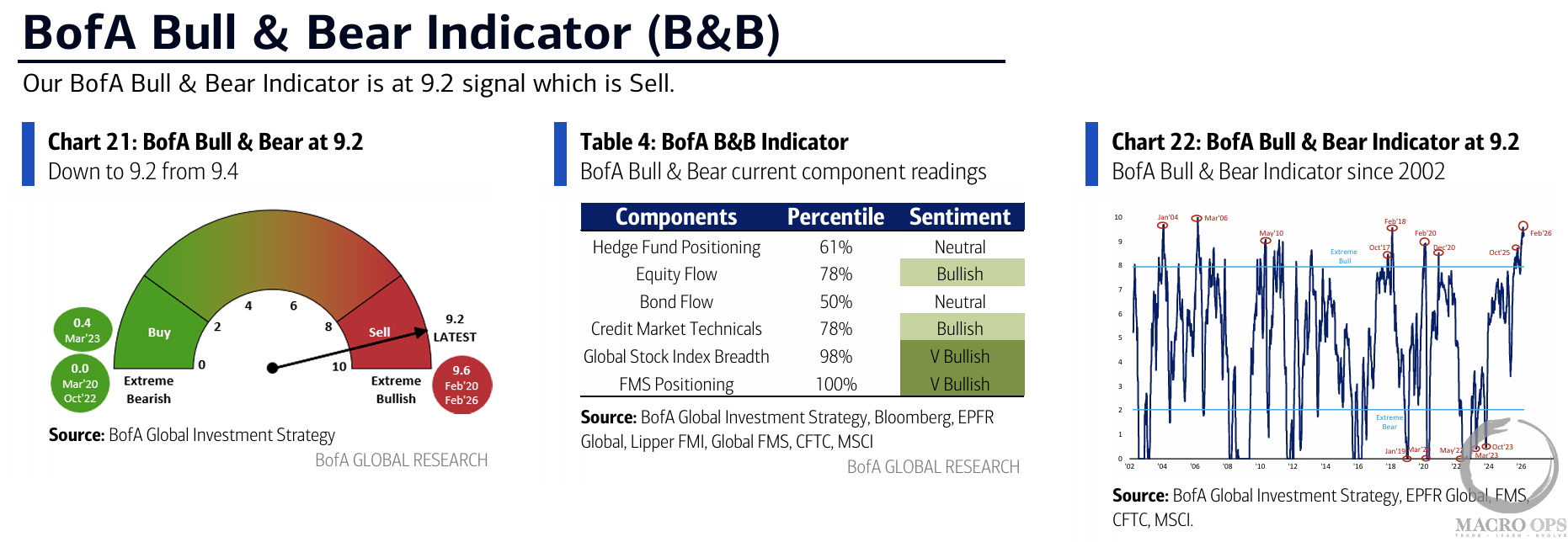

6. Our Trend Fragility indicator has come down to the 68th %tile. BofA’s Bull-Bear climbed last week to a recent high of 9.2 — still well into Sell Signal territory. I expect a full reset in both over the next month or two.

Macro

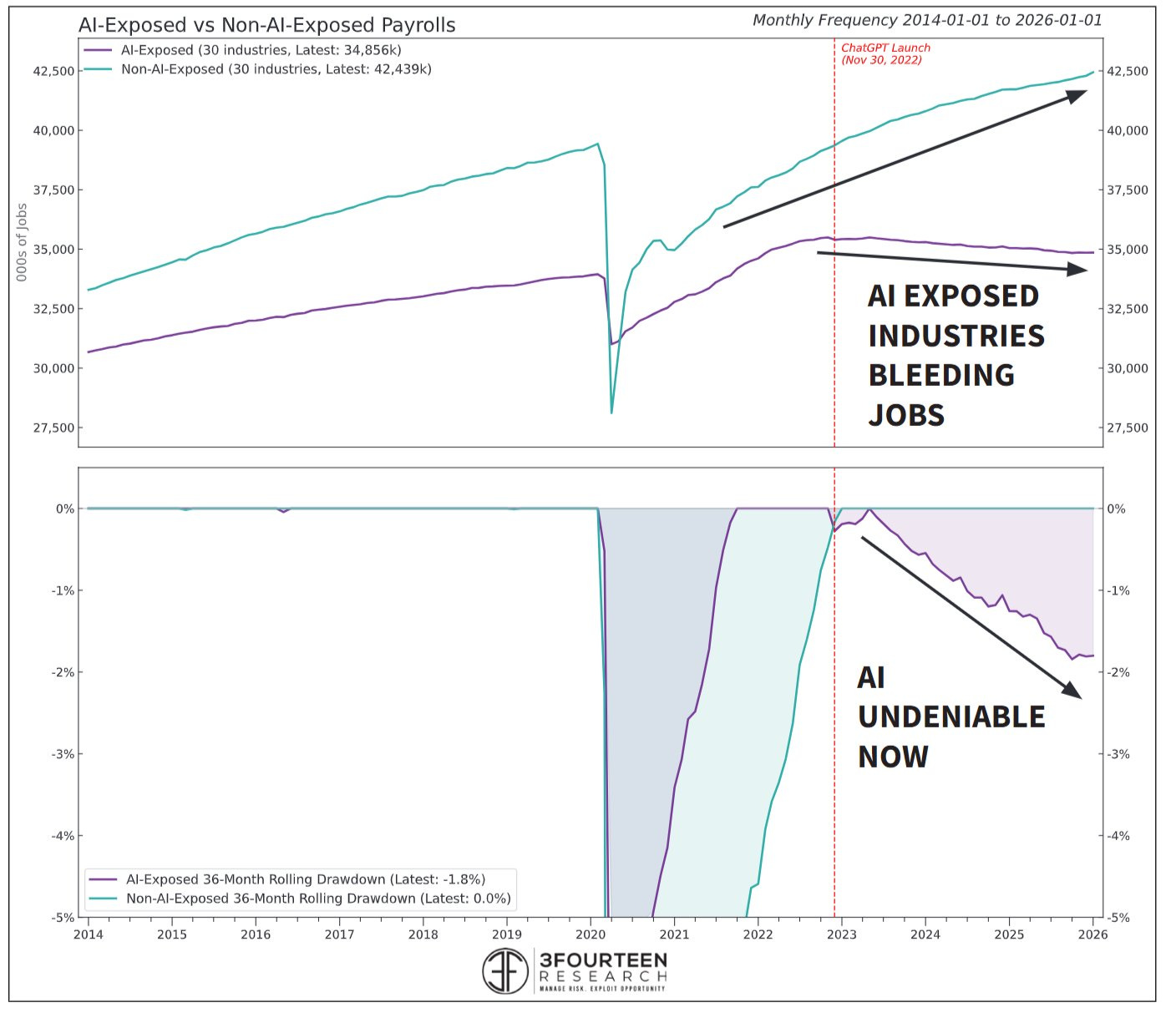

7. AI’s impact on labor, software, credit, and a host of other things continues to be a key market driver. I’m tracking the debate closely. Here’s @WarrenPies’ recent take:

“AI’s impact on the labor market is no longer theoretical. In the most AI-exposed industries, job losses are accelerating — especially relative to pre-AI trend growth. AI-resistant industries continue to add jobs. As the year progresses, expect that wedge to grow.”

8. On these debates, I try to keep an open mind — find the most cogent and honest thinkers on both sides, then track their arguments against the data and what the market is actually saying, while always keeping a pulse on where the Narrative Pendulum sits. Here’s Citadel Securities with a good counter:

“It seems more likely that AI will be a complement rather than a substitute for labor in many areas. Historically, technological revolutions have altered task composition rather than eliminated labor as an input. To produce a negative demand shock large enough to overwhelm output expansion, one must assume near-total automation of economically relevant labor combined with extremely weak redistributive responses. To frame this debate correctly, simply ask: was Microsoft Office a complement or substitute for office workers? Ex-ante, the concern skewed toward substitution. Ex-post, it appears a clear complement.”

Here’s the link to the full piece.

9. Whichever side ends up being right will have profound implications for markets. The AI-eats-most-jobs scenario is obviously deeply deflationary. The other is potentially quite inflationary. Our models continue to point to falling inflation over the next three months or so, with a potential hockey-stick turn somewhere in the second half of the year. This chart from BBG’s Simon White seems to corroborate that — Truflation (blue) collapsing while his inflation lead (yellow) trends up.

Trade Setups / Topical Charts

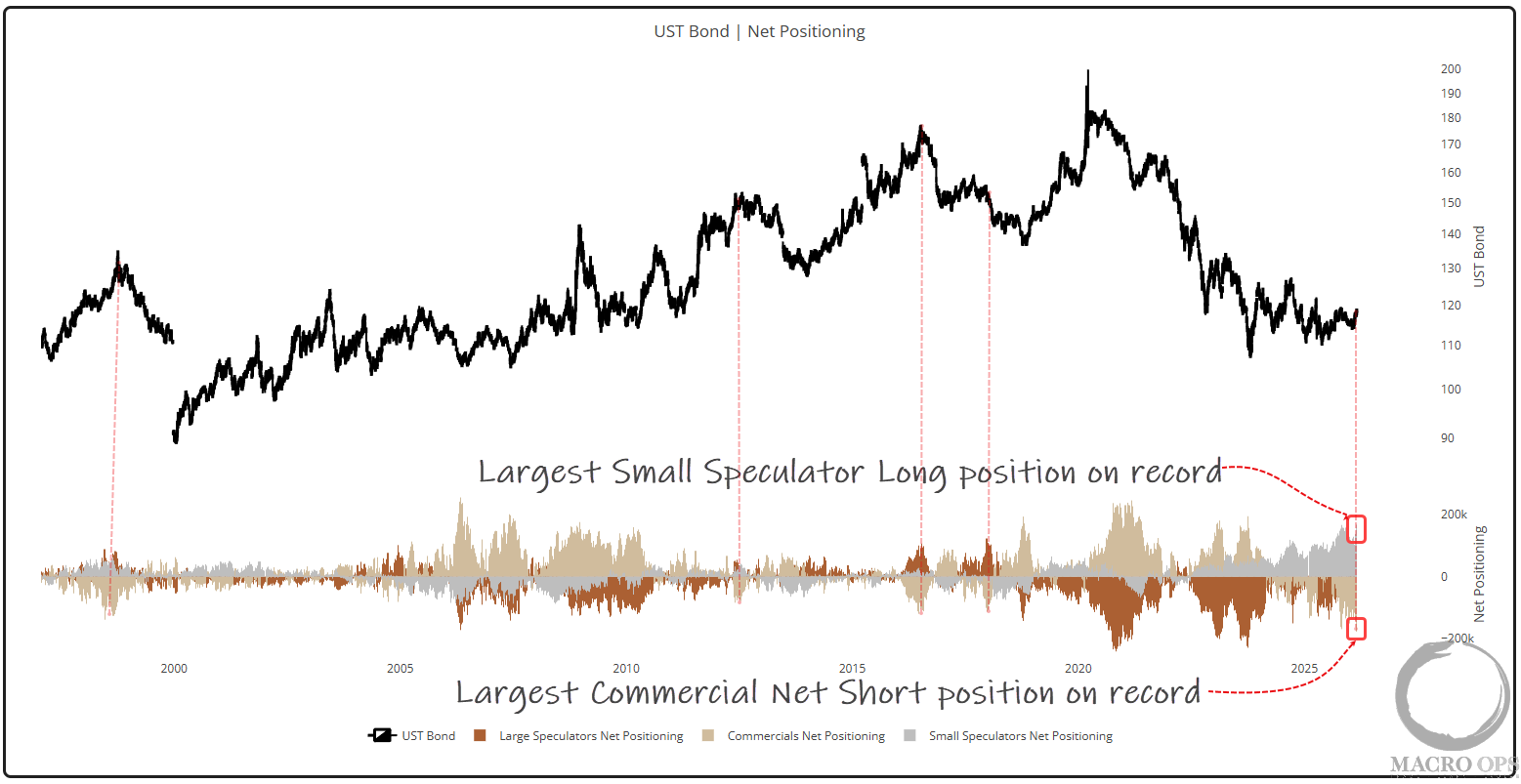

10. Honestly, the rally in the long end over the past month has surprised me. Last week, 10s punched through 4% for the first time since October. The AI narrative has been driving it — but in my opinion, the move looks overdone, and the long end looks expensive. Small Spec positioning in long bonds is at its highest level in history, while Commercials hold record shorts. The vertical red lines mark past instances where Commercials moved to large net short positions — it tends to be followed by a significant move lower.

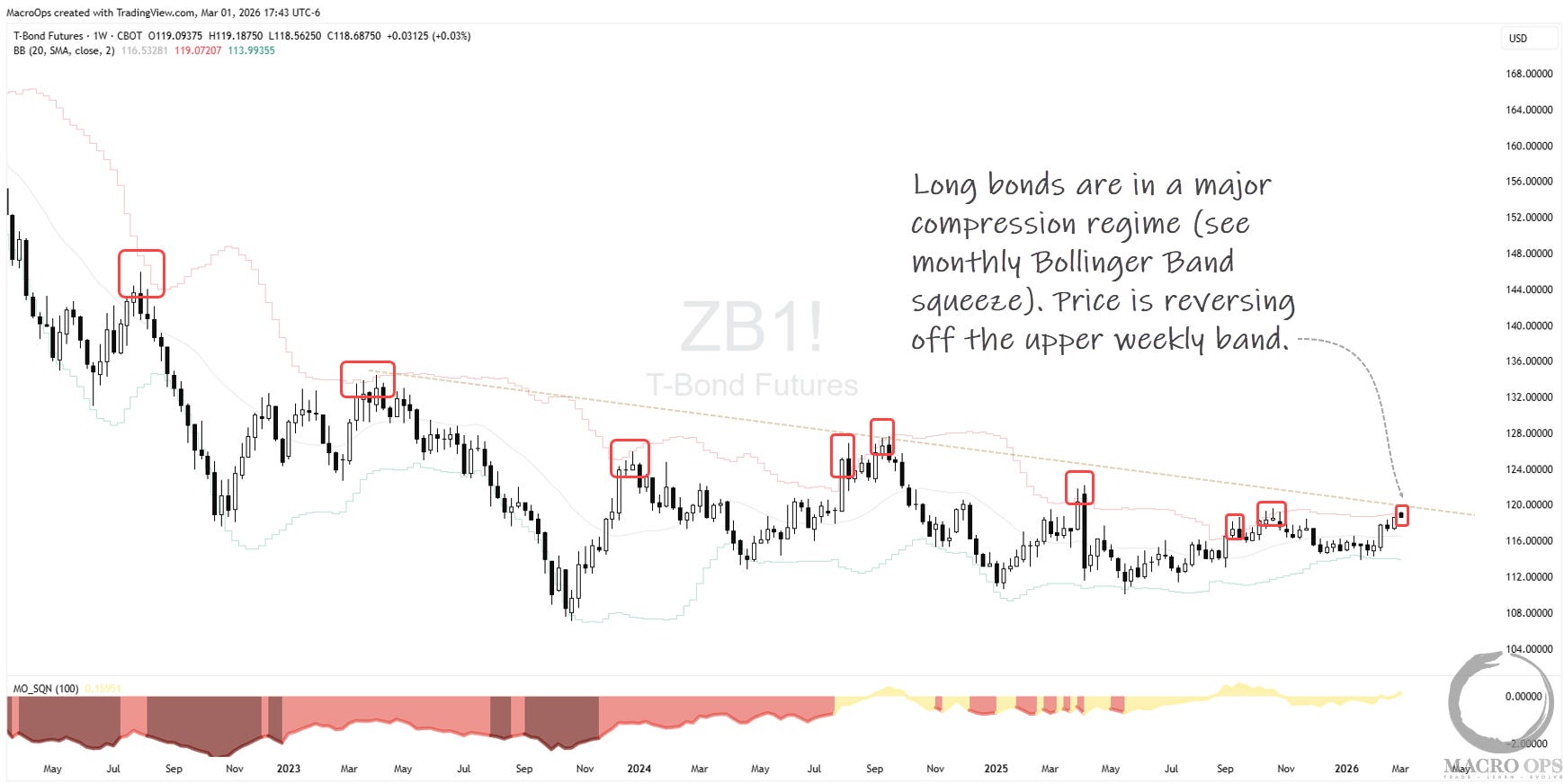

11. I’m looking for a potential short here against our long on the front end. The weekly ZB chart shows price reversing off its upper weekly band and downward trendline — a technical ceiling that’s held many times over the past few years.

The long end is also in a major compression regime (pull up a monthly Bollinger Band width chart). Like the front end, this tells us a big move is coming. My bet is that move is lower.

12. Check out this weekly chart of Moderna (MRNA). It broke out from a 12-month rectangle in mid-January and cleared its recent consolidation last week. Our resident systematic chartist, Mike ,G first flagged the setup on January 17th (link) — also, here’s the link to Mike’s latest. It’s definitely worth a read.

I continue to like biotech. It’s showing solid relative strength. We added JAZZ last week and will likely add MRNA in the coming days.

Join The Collective

Thanks for reading.

Your Macro Operator,

Alex