A colleague of mine told me about the risk manager he worked under. The relationship sounded downright abusive.

The manager would constantly watch over his shoulder, critiquing every chart analysis and order entry. “Everyone else on the floor is having a great month … what’s your problem?” he would ask.

When a trade would stop out, there was the manager again: “That was a dumb place to put your stop. Of course it got run.”

The manager never left my colleague’s side. Always pointing out what he could have done better, framing a profitable trade as a gift from the heavens, blaming losing trades on his incompetence.

He tried to motivate through criticism, shame, and pressure. This made the manager terrible at his job.

My colleague was more uncertain in his trade plan, more anxious in his order entry, more focused on avoiding the next verbal thrashing than on creatively adapting to the market environment and professionally stewarding the firm’s capital.

I told him he had to fire that manager. Find a new one within the firm. Or move firms entirely.

He told me he couldn’t. Because wherever he went, the manager would follow.

The manager didn’t work for the firm. The manager was the voice in my colleague’s head.

Most people battle with their inner critic. They try to silence it, argue with it logically, suppress it. This only entrenches its authority.

The real issue isn’t the voice. The issue is believing it’s an effective manager.

See through this fallacy. See that the voice is driven by fear. That it hasn’t improved your trading one bit.

Then, give that manager the performance review he deserves, and fire him.

Trade Tactics for Bear Markets

Last week, when I shared a chart depicting my long equity regime filter closing, a member of The Collective asked if I simply inverted my trade tactics for bear markets.

My response: “I wish it were so simple …”

Bear Market declines in equities are not the mirror reflection of Bull Market advances, as much as I’d like them to be.

Two things work against trading equities to the short side in Bear Market Regimes: 1) the volatility of the regime and 2) the math of short-side trading.

Let’s start with the math.

On the long side, the math works with you. A $100 stock moving to a measured move target of $130 in three $10 legs requires 10%, then 9.1%, then just 8.3%. Each leg gets easier. Each dollar gain is a smaller percentage ask. Momentum compounds favorably.

On the short side, the opposite is true. That same stock falling that same $30 measured move requires 10%, then 11.1%, then 12.5%. The market must accelerate in percentage terms just to sustain the same dollar move.

While stocks can crash dramatically in percentage terms, maintaining a large dollar move to the downside means the percentage hurdle keeps rising at every step.

And as traders, we are paid by dollar moves.

This asymmetry makes simply flipping a long setup to a short one a more mathematically challenging trade.

This is also why the old saying, “stocks take the stairs up and the elevator down,” is only partially true in percentage terms.

Which brings us to the second major difference about Bear Market Regimes: volatility.

In the Classical Charting bible, Technical Analysis of Stock Trends, Edwards & Magee note that “[Bear Market] down trends are far less regular and uniform in their development than Bull Market advances.”

A figure early in the book highlights a prominent price action feature of Bear Markets: “’Rounding patterns’ [...] typical of rallies in a Primary Bear trend.”

The sustained Bear Market of 2022 exemplified this pattern beautifully:

Far from the “regular and uniform” Bull Market advances, these Rounding Patterns wreak havoc on breakout entries.

Individual equity names will breakdown coincident with a swing low breaking in the indices:

The weakest stocks will make progress toward their measured move targets. The most resilient will just poke through the lower boundary of their consolidations.

Both happen right before a screaming rally back toward the long-term moving average:

I’ve found that these massive rallies, which form the crest of each Rounding Pattern, can stop out even the best looking short setups.

So, as traders, we have to adapt to these market conditions, and adjust our tactics for the Bear Market Regime.

Looking at the charts above in hindsight, the worst place to have shorted would have been in those red boxes. And the worst place to long? The green boxes.

Consider instead: going long in the red boxes and short in the green boxes.

Do not mistake what I’m suggesting as trying to bottom fish or top tick. These are a fool’s errand.

Instead, if we understand that short setups fail and reverse in the red boxes … why not long a failed short setup in this regime, targeting the opposite side of the range?

And if long setups fail and reverse in the green boxes … why not short a failed long setup in this regime, targeting the opposite side of the range?

I’ve found these tactics to be far better suited to Bear Market Regimes than simply inverting my long-side tactics built for “regular and uniform” Bull Market advances.

When the environment is different and the math is different, the tactics, too, must adjust.

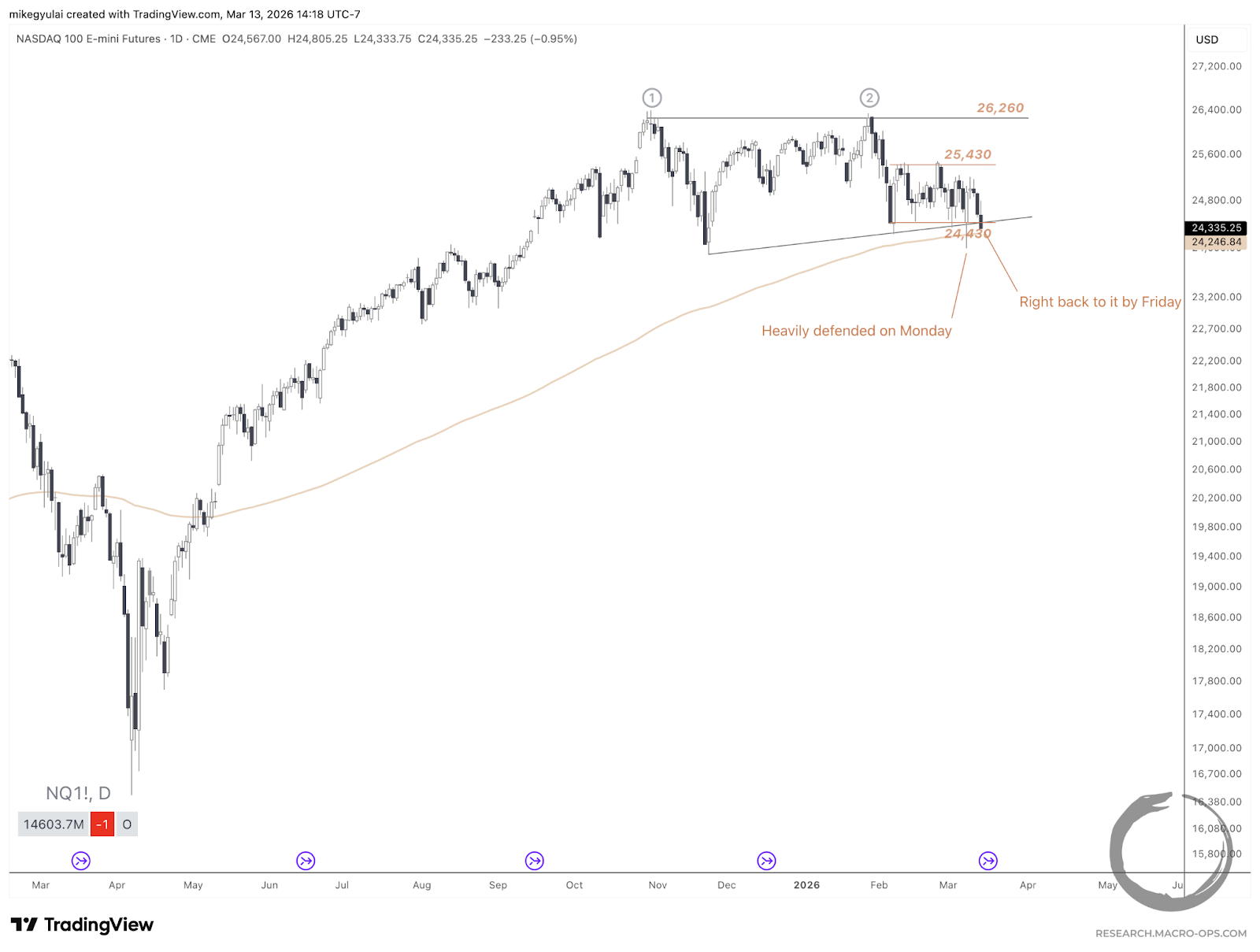

Nasdaq’s Roundtrip

In last week’s issue, I covered the consolidation in the NASDAQ between roughly 25,430 and 24,430. I mentioned that this one-month consolidation stood right at the convergence of the (potential) Ascending Triangle’s lower trendline and the 200EMA, which would warrant any breakdown meaningful.

Monday saw the 25,430 level vigorously defended, further showcasing its importance for market participants. By Friday, we round tripped right back to it.

The Nasdaq-100 Equal Weight continues to look like an underside retest of a breakdown.

Expect heightened volatility around the 200EMA of NQ next week. The level has proven significant to market participants, and those who defended it are now under real pressure.

The Pauses That Refresh

There are a number of opportunities to play on the short side or between range boundaries next week.

Here are the names that grabbed my attention:

Active watchlists, real-time trade alerts, and live portfolio tracking are reserved for members of The Collective, our premier service offering discussions on high-level theory and performance, differentiated research, and a global community of serious traders and investors dedicated to mastery. Learn more about The Collective here.